October 17, 2023

Summary

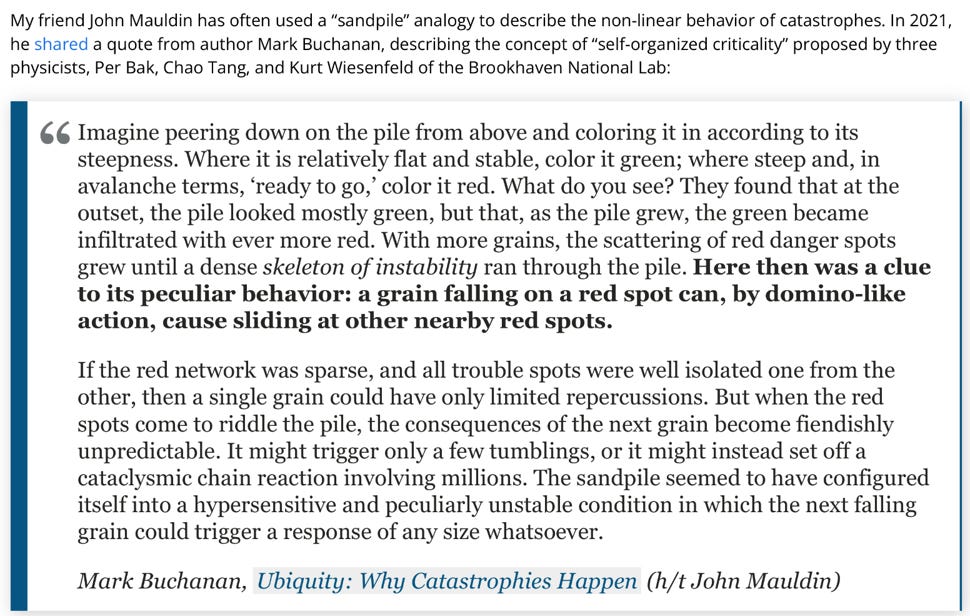

On stable instability

No convexity is not a dirty word

Households growing despair

Housing, crack appearing

Credit divergences

Breadth is outright ugly

A valuation journey

Many Japanese companies are underfollowed

Macro – Instability

We have dedicated our MashUp’s to the quest of the red spots, Mark Buchanan describes here below. There are too many to be ignored!

Sometimes it is better to be out of the markets wishing to be in, rather than in the market wishing to be out, especially when you are paid >5% for your patience.

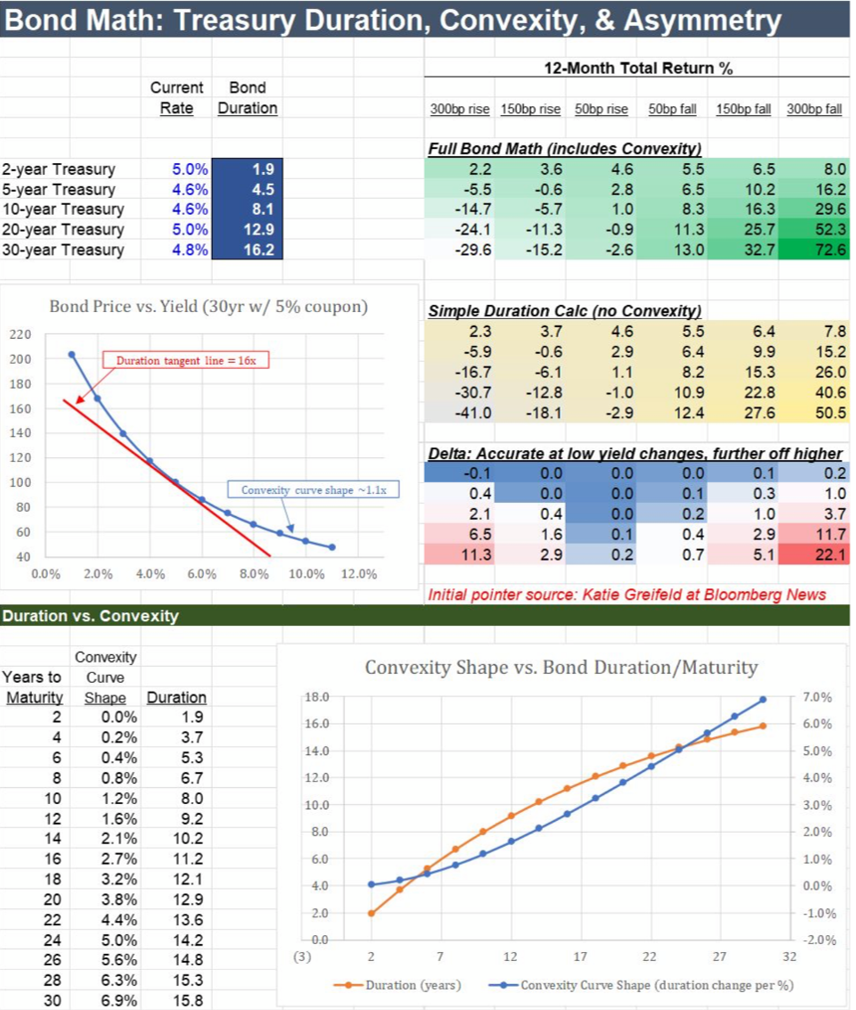

Macro – Bonds Convexity

Before we start the Macro section in earnest, we wanted to make sure that anyone would see the following graphs/tables on the current convexity of the fixed income markets. For investors who only have been in the markets for less than 15 years it is only an academic experience…

For the current situation we first start with this beautiful illustration courtesy of Rick Falk Wallace.

The second illustration is from BoA. We would wait before committing any capital to their most aggressive example…

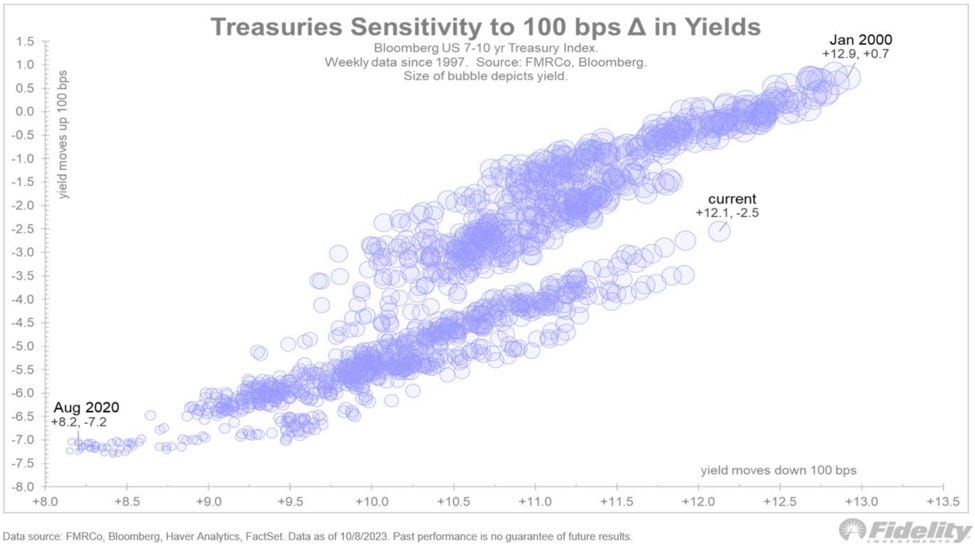

The third and last illustration is how convexity for the 7-10 yr Treasury Index has evolved since 1997…

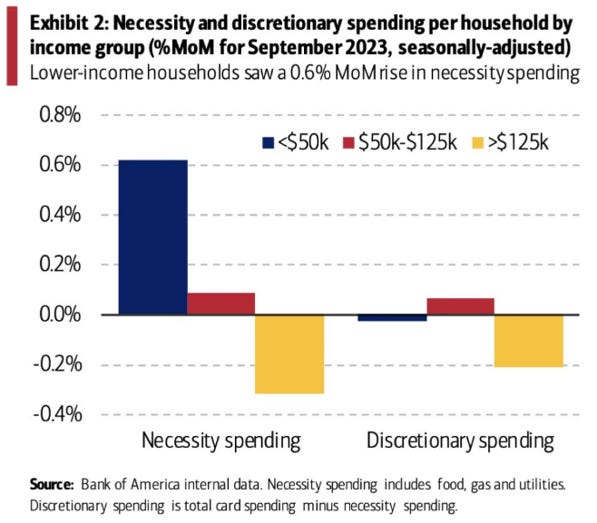

Macro – Households

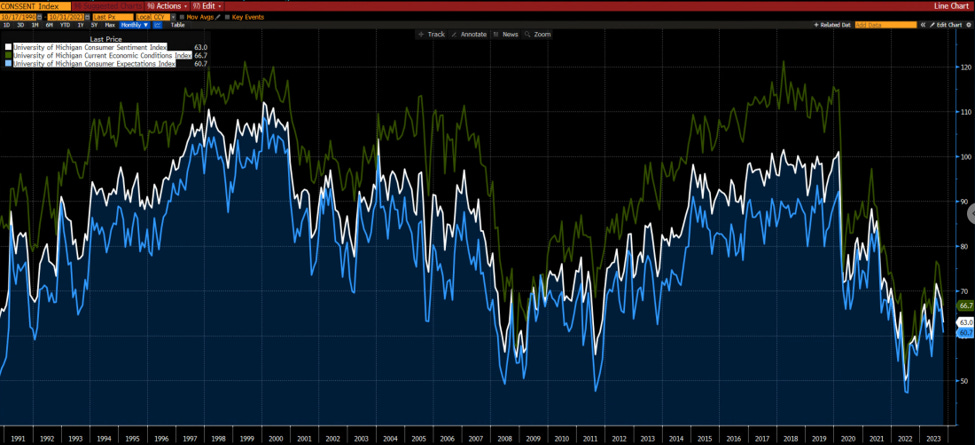

Our scenario is slowly developing with consumer confidence taking another leg down.

The lower income households must spend more on food, gas and utilities while higher income households are just starting to adjust to their loss excess savings and hence are starting to substitute what they put in their “necessity spending” (lower income households did it months ago and their spending is now evolving with inflation)

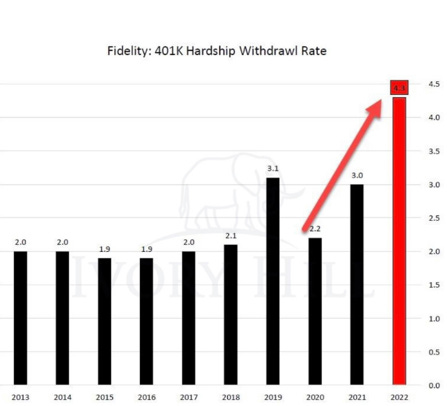

Macro – Households - Employment

We are also seeing the tense situation of many households with the rapid increase in 401K hardship withdrawal.

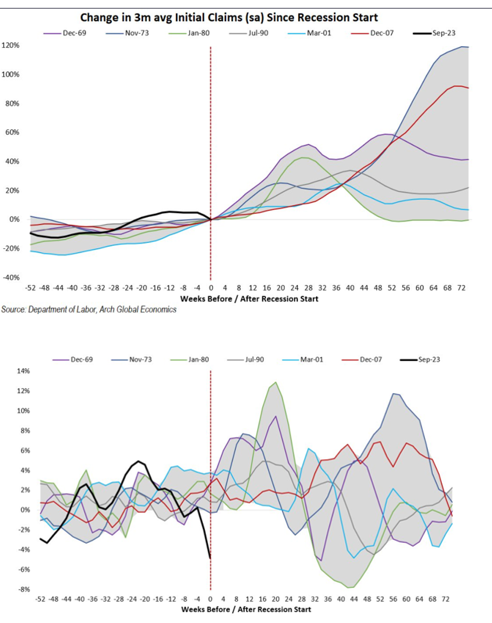

One of the rare employment indicator with a good historical record at business inflections which has yet to confirm our “job market weaker than it seems” thesis are the “Initial claims” numbers.

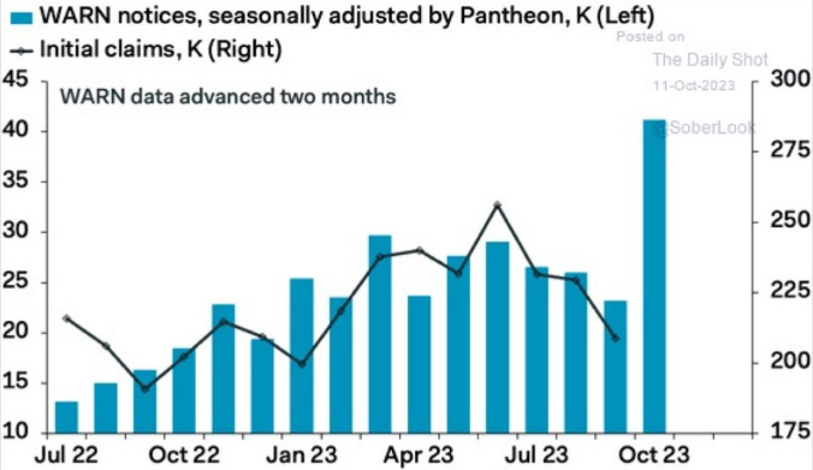

Warn notices seem to indicate that this will change soon.

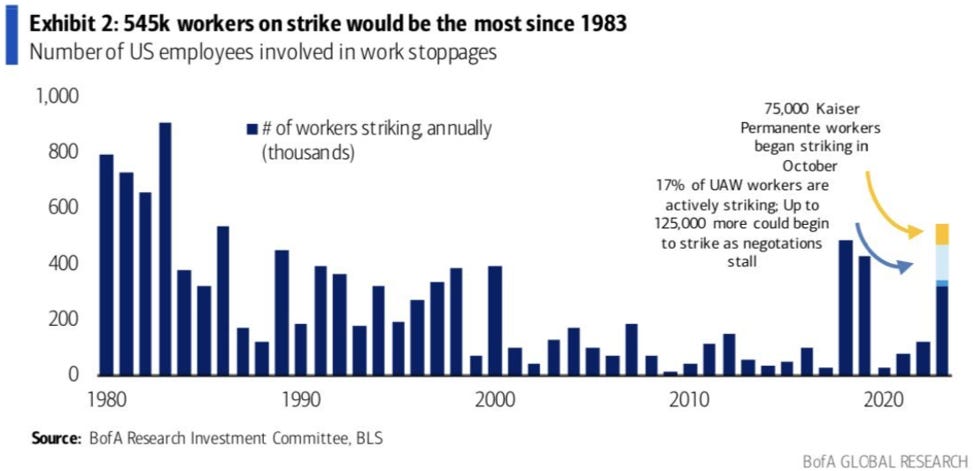

Before we close this “Employment“ section, we want to put again a graph illustrating the potential change in dynamics of labor activism in the US. This might have (our view is that it will) profound implications on the future profitability of corporations in the future.

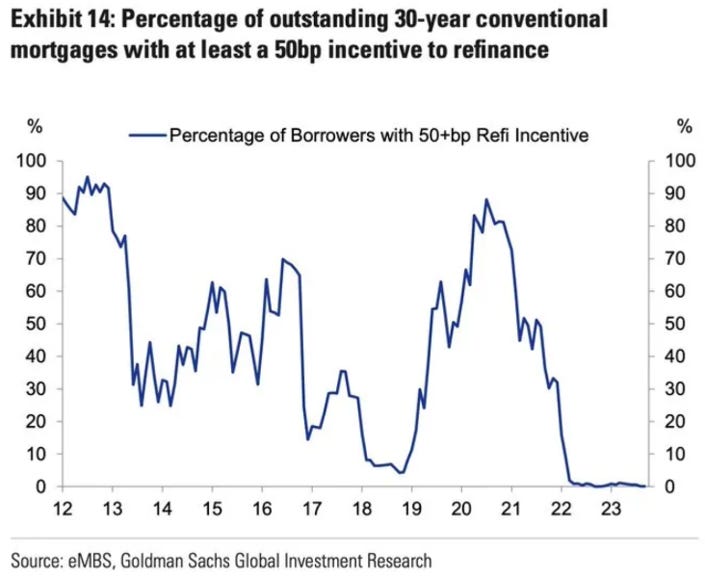

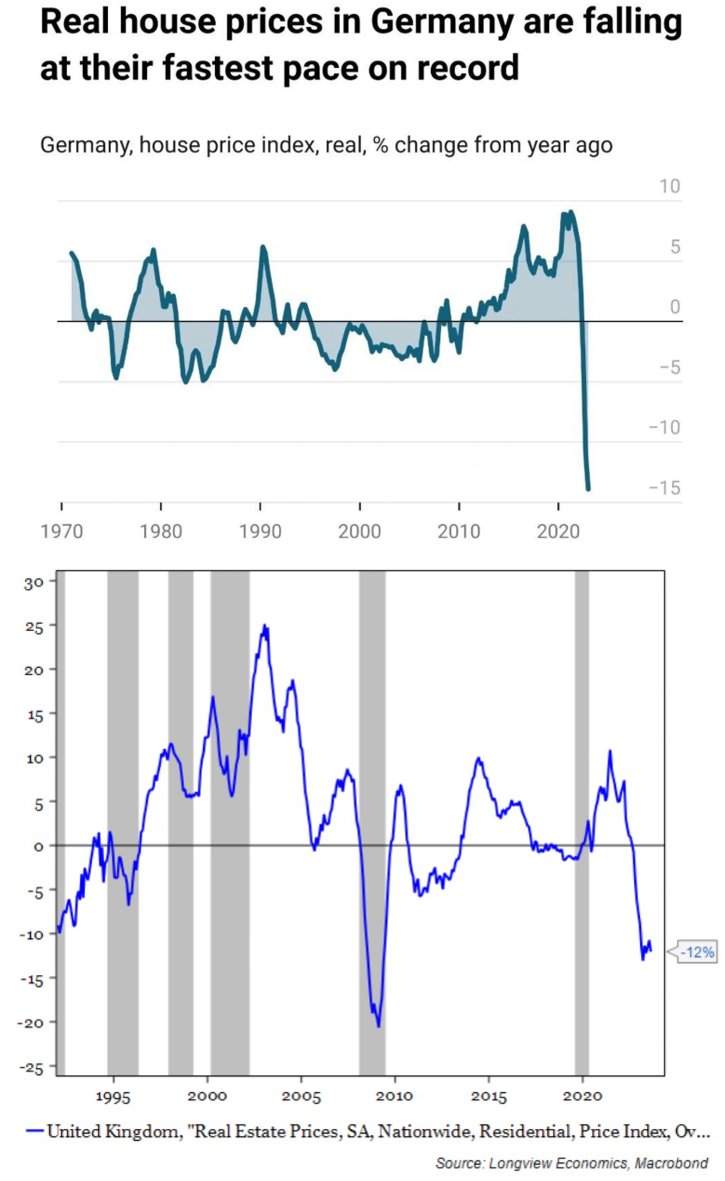

Macro – Housing

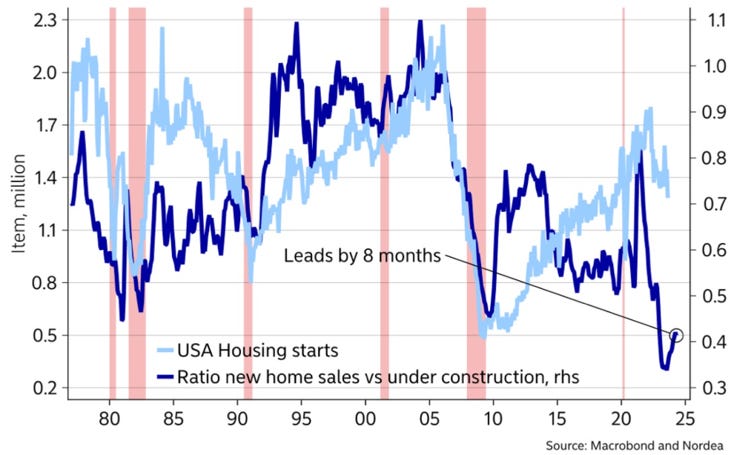

We have argued that there are too many houses being built in the US given current mortgage rates and macro prospects. If we add the incoming supply of “short rentals”, which were primarily financed with adjustable-rates mortgages, inventories are likely to surprise to the upside in the next 12 months.

In the meantime…

The current situation is of course much worse in countries where mortgages have shorter-duration on average and are harder to refinance…

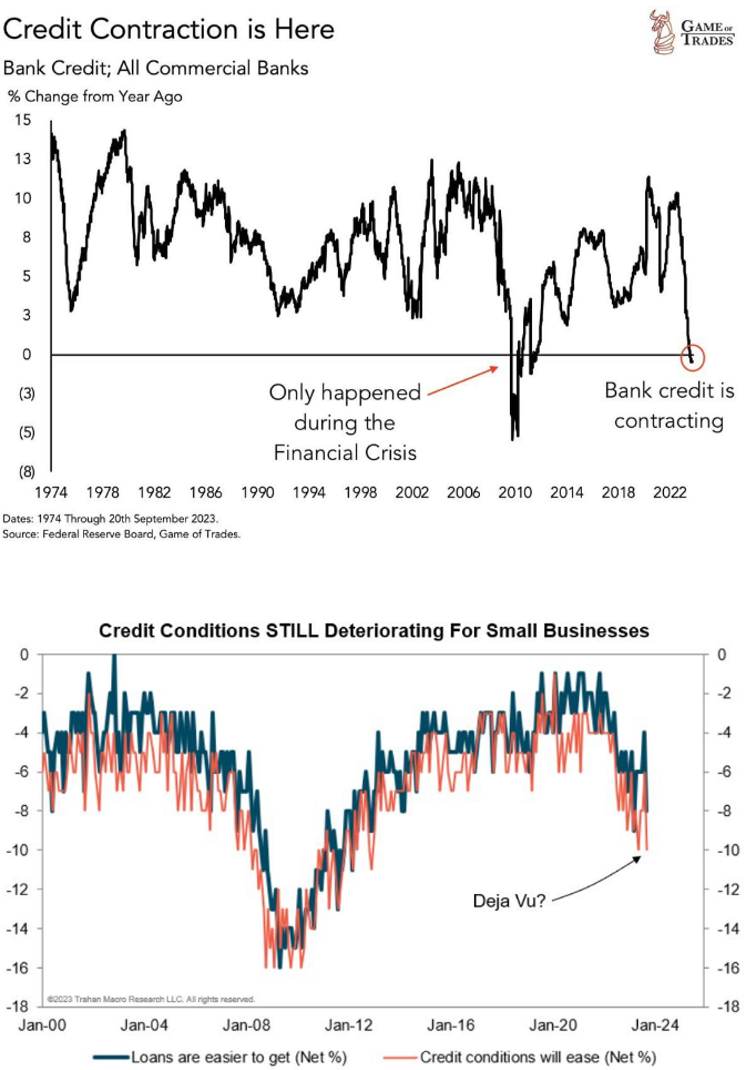

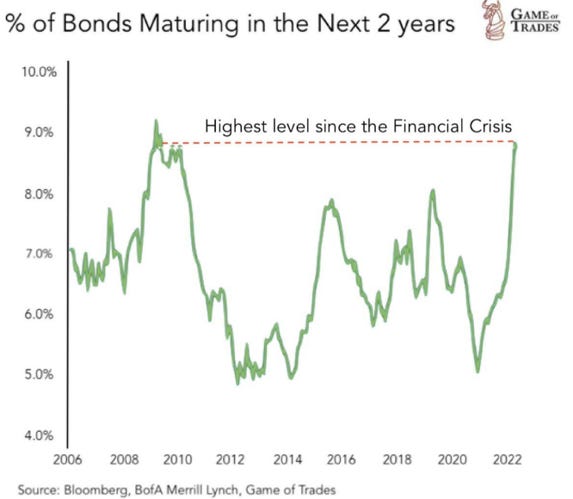

Macro – Corporate - Credit

Credit is harder to get as confirmed by both hard and soft data…

… at the same time the % of bonds maturing in the next 2 years is reaching GFC level (back then it was because companies could not borrow, today some can not but most choose not to, hoping that the Fed will soon lower rates…)

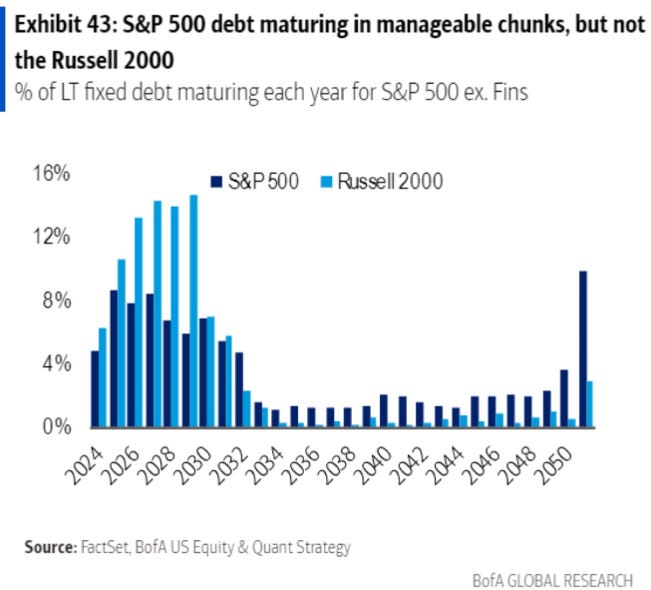

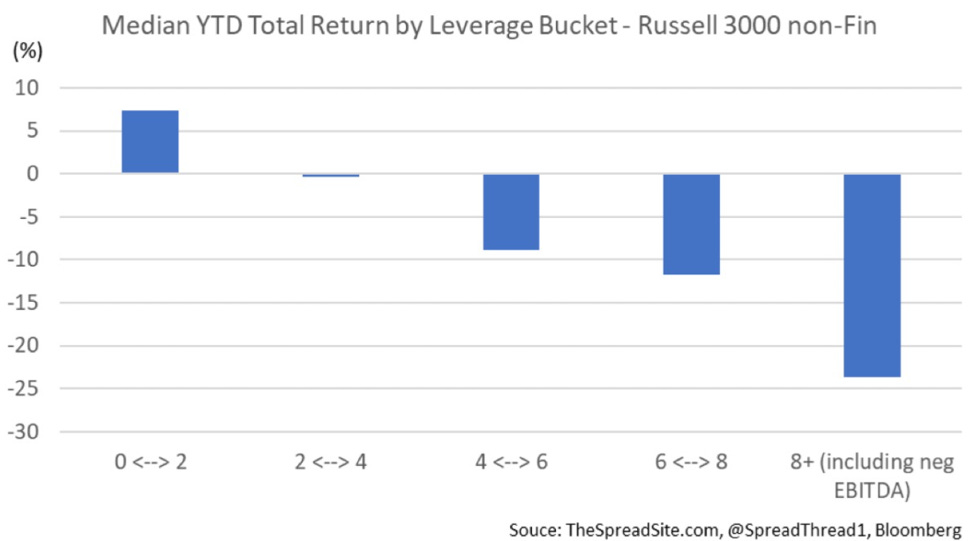

Not all companies are in the same situation though…

This can also be seen here…

The market has taken notice!

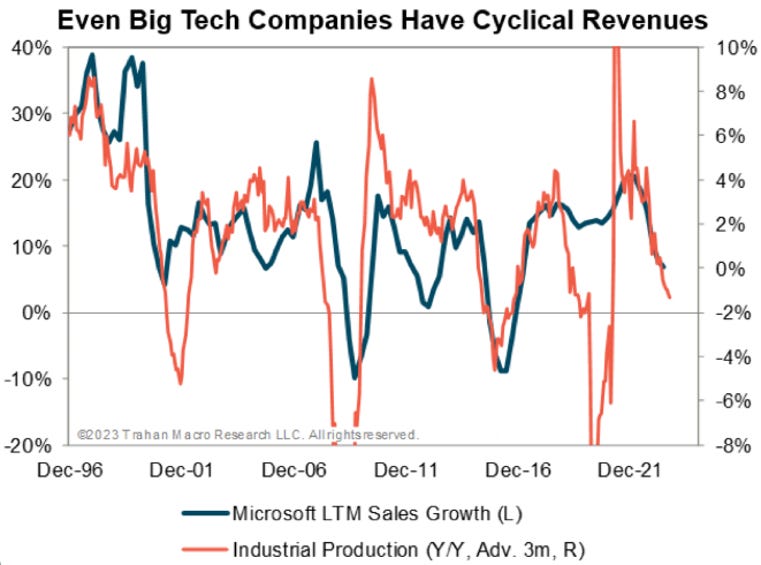

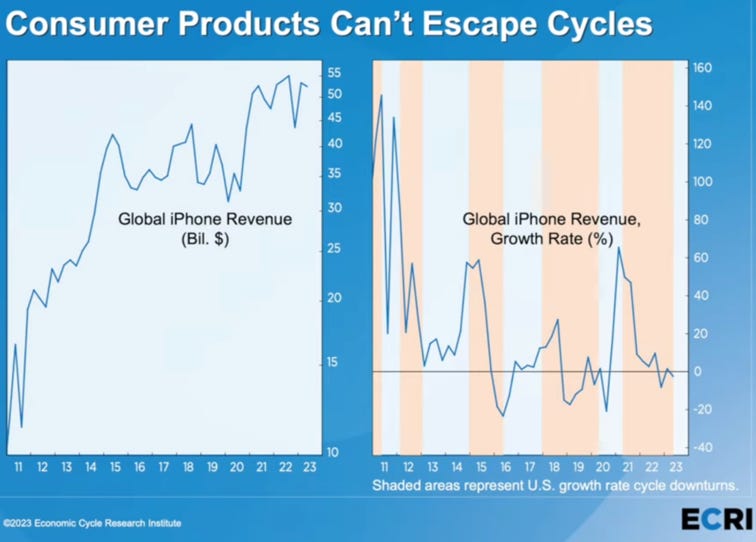

Macro – Corporate - Cyclicality

Even the highest quality companies experience some cyclicality in downturns as the market seems to be forgetting time and time again.

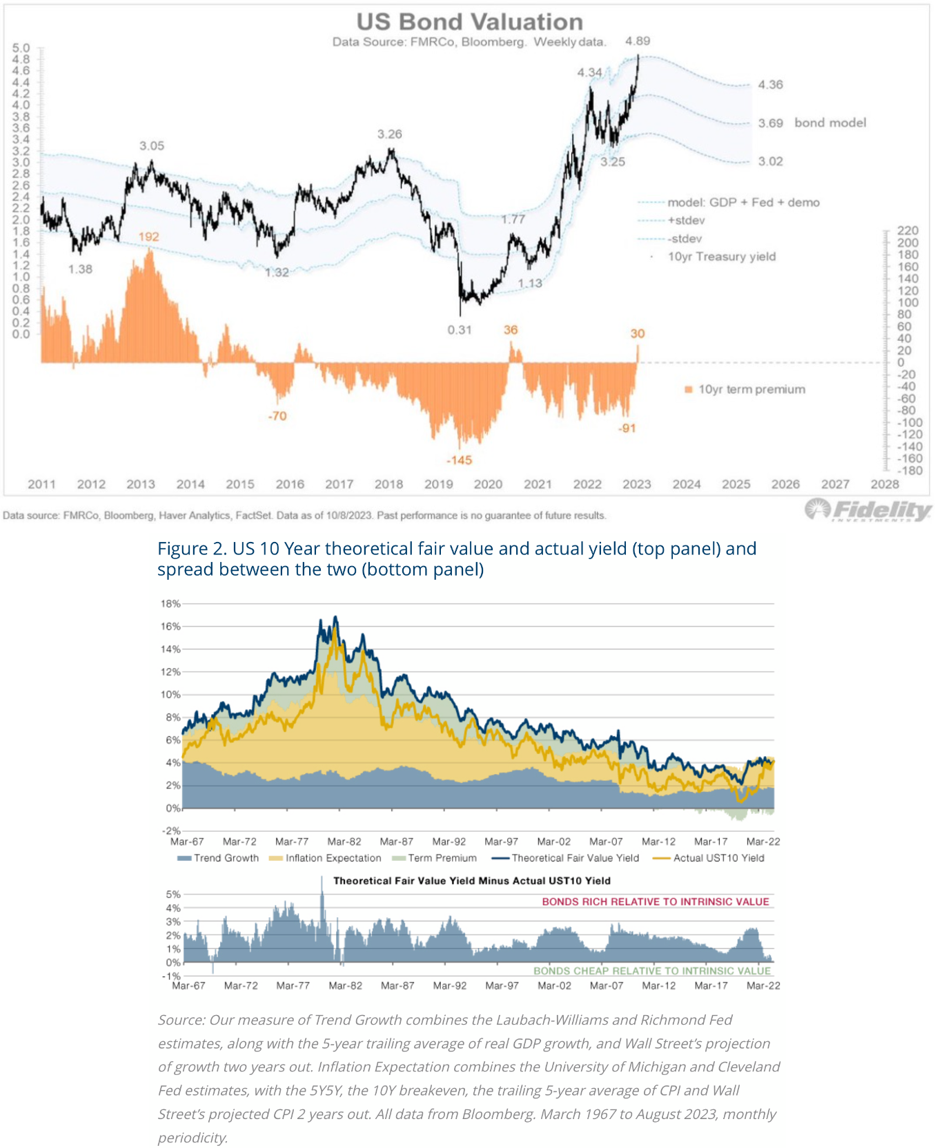

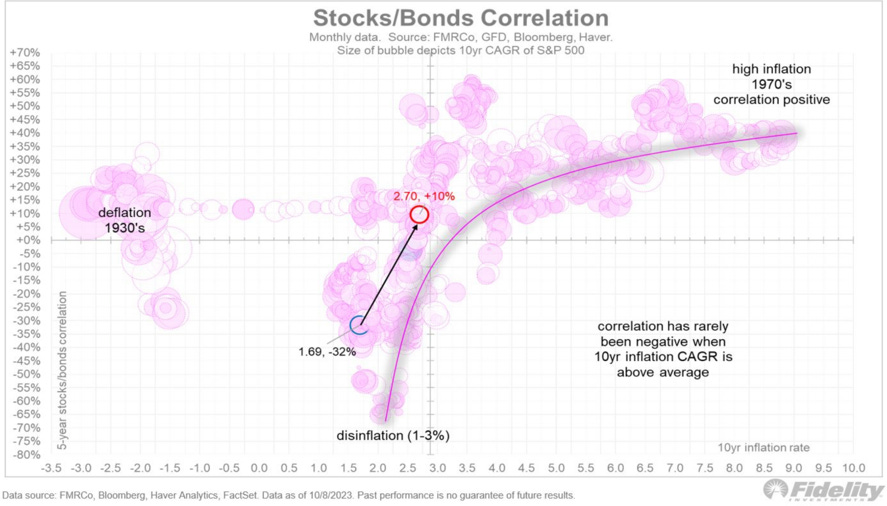

Market – Bonds

Last week we presented J. Hussman Bond valuation model which indicates that US Govies were reaching fair value. Today we present Fidelity’s J. Timmer and Man Financial ones. Same conclusion.

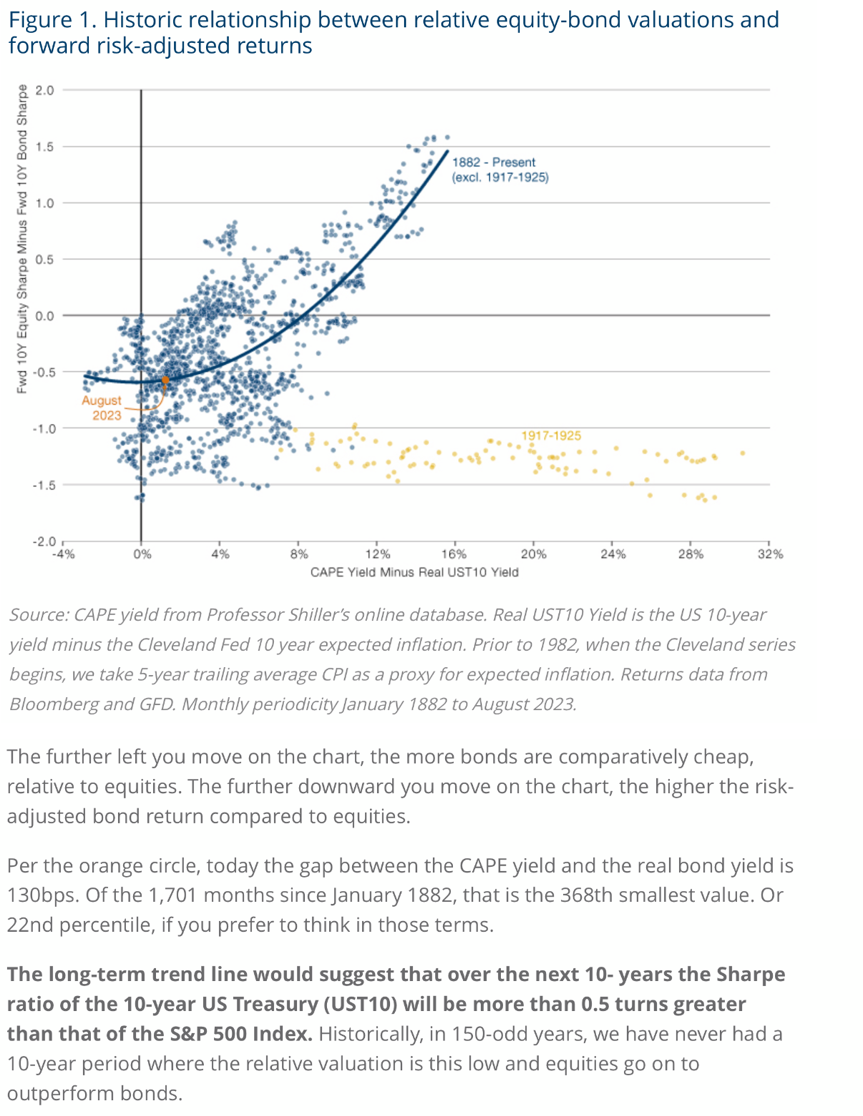

Man also compares stock and bond valuations. Their conclusion is that the 10 years US Treasuries will have a Sharpe ratio 0.5 higher than stocks.

Given the current positive correlation of stocks to bonds which we expect to turn negative at least during the initial phase of the recession, we would recommend to explore option based relative-value strategies.

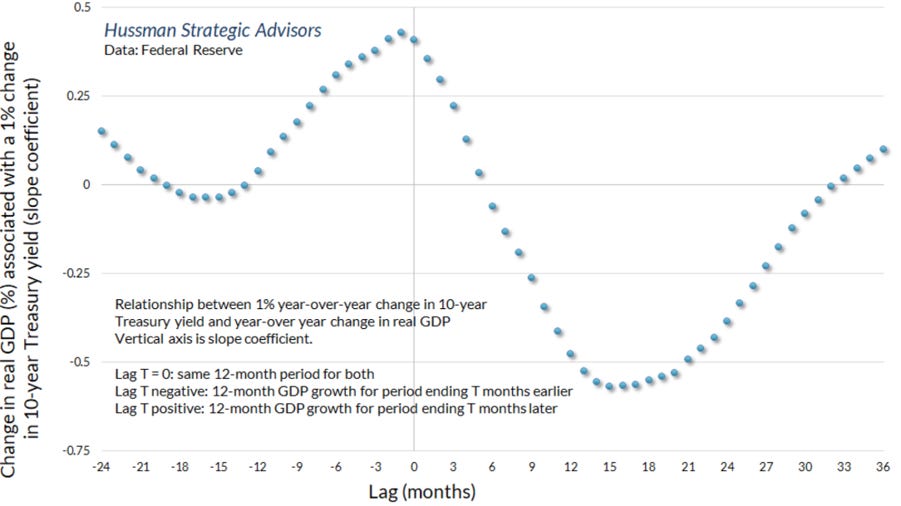

The recent rapid increase in real yields will weight on growth for at least the next 15-18 months…

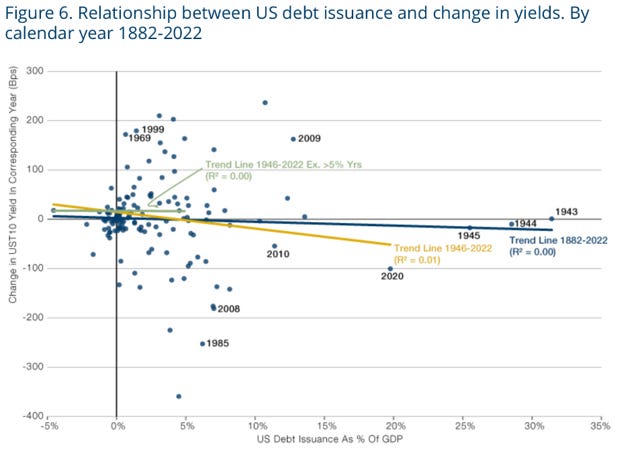

Two graphs to finish this section.

First the debate on the relationship between debt issuance and change in yields is not yet settled. Man thinks if there is a relationship it is the inverse of the expected one…

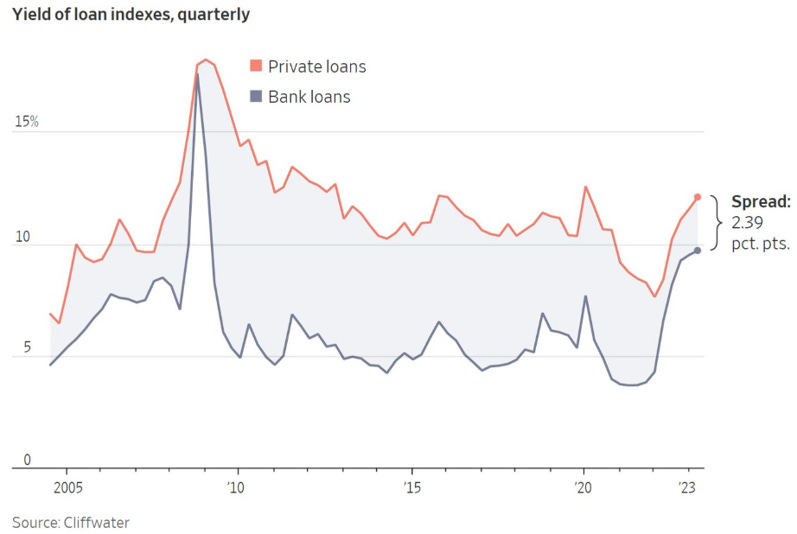

The second one is on the spread between private and bank loans... Is too much capital flowing to private debt just when it could be tested for the first time in a conventional recession?

Market – Liquidity

Buybacks, the major fuel of the past 15 years US market valuation expansion, are not expanding anymore. Our contention is that even the magnificent 7 will have to lower the amount of money they plow into the markets to buyback their own shares in the months to come.

Valuation-agnostic strategies have been selling.

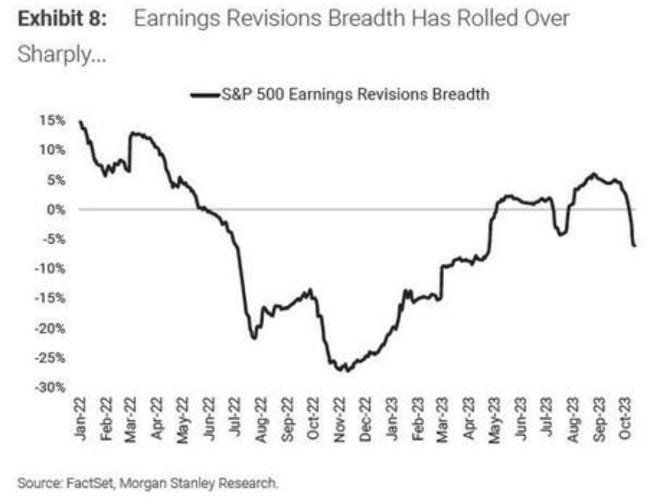

Market – Breadth

Breadth continues to indicate that the move which started a year ago is a bear market rally and not a new cyclical bull market.

Another way to look at it. There is no uniformity in markets actions.

And now even earning revisions breadth for the S&P 500 is reversing…

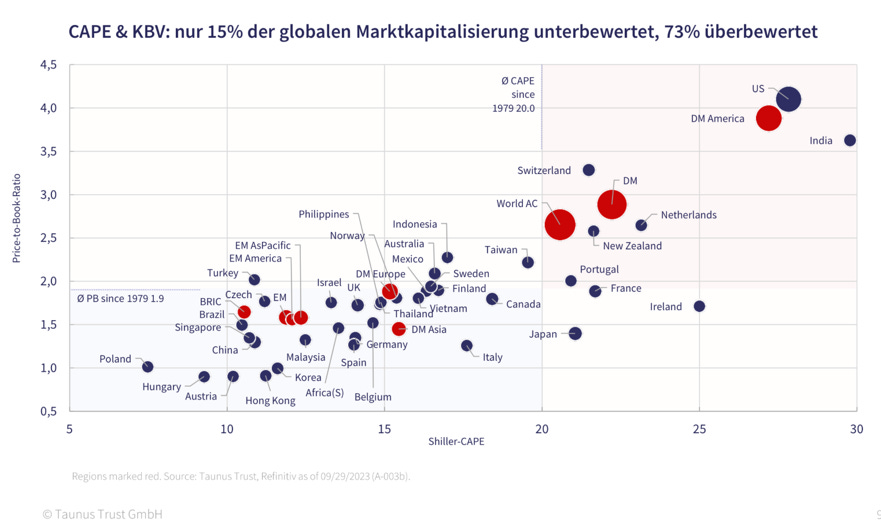

Market – Valuation

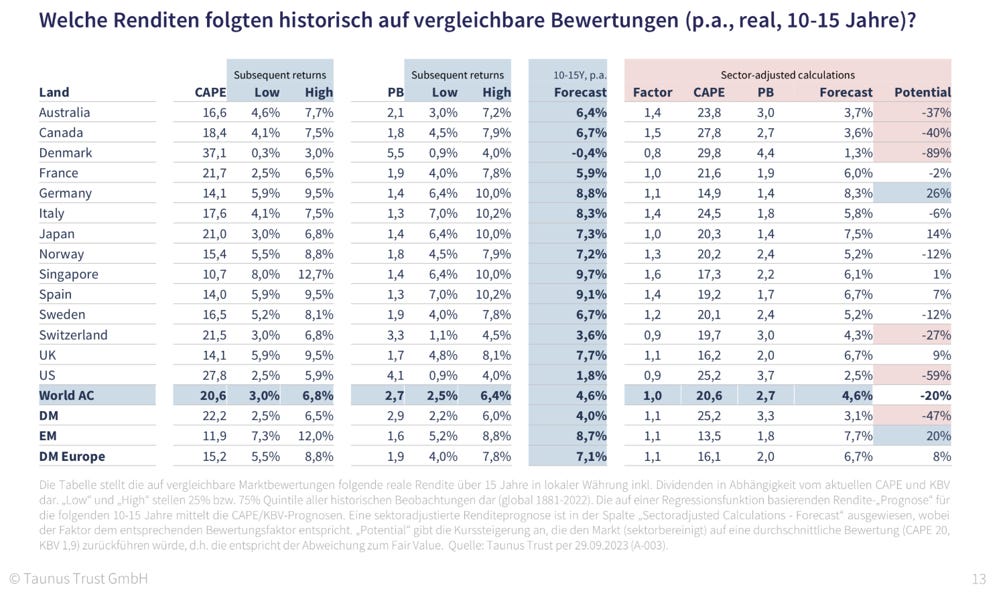

The first part of the valuation section will be based on the excellent work of N. Keimling from Taunus Trust.

Looking at today’s global market valuation, he estimates that only 15% of the global market cap is undervalued and 73% overvalued. This is a time to take big contrarian relative-bet and have the courage to sit through short-term volatility.

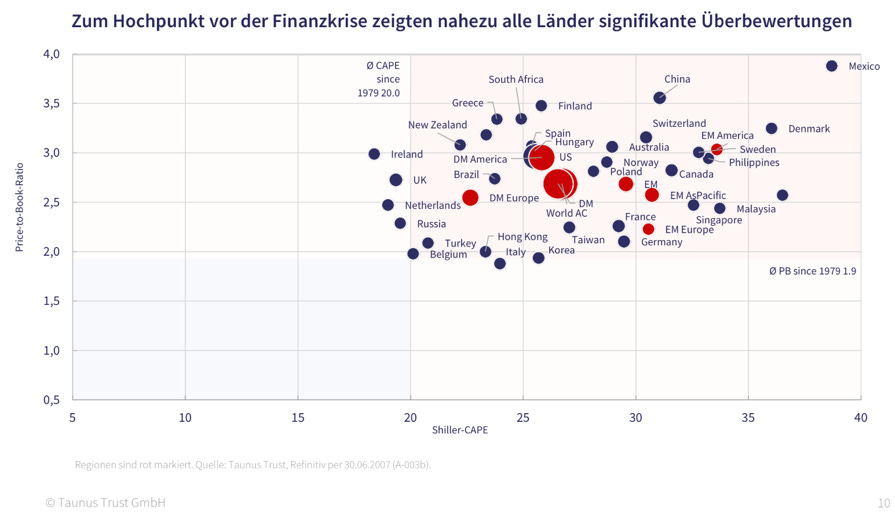

To compare here is how the markets were valued in 2007 pre-GFC. Not many places to hide.

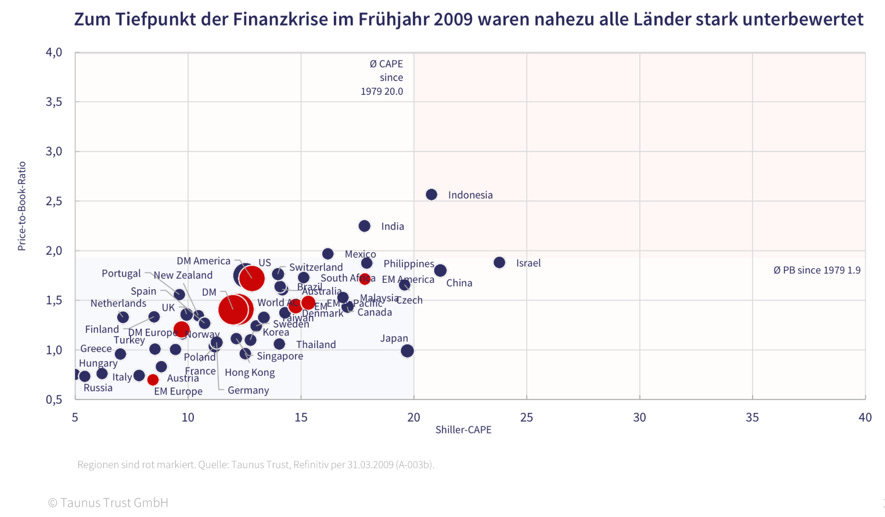

Early 2009, to paraphrase W. Buffett one would have felt “like an oversexed man in a harem”.

Here below you will find where various markets stand according to his methodology.

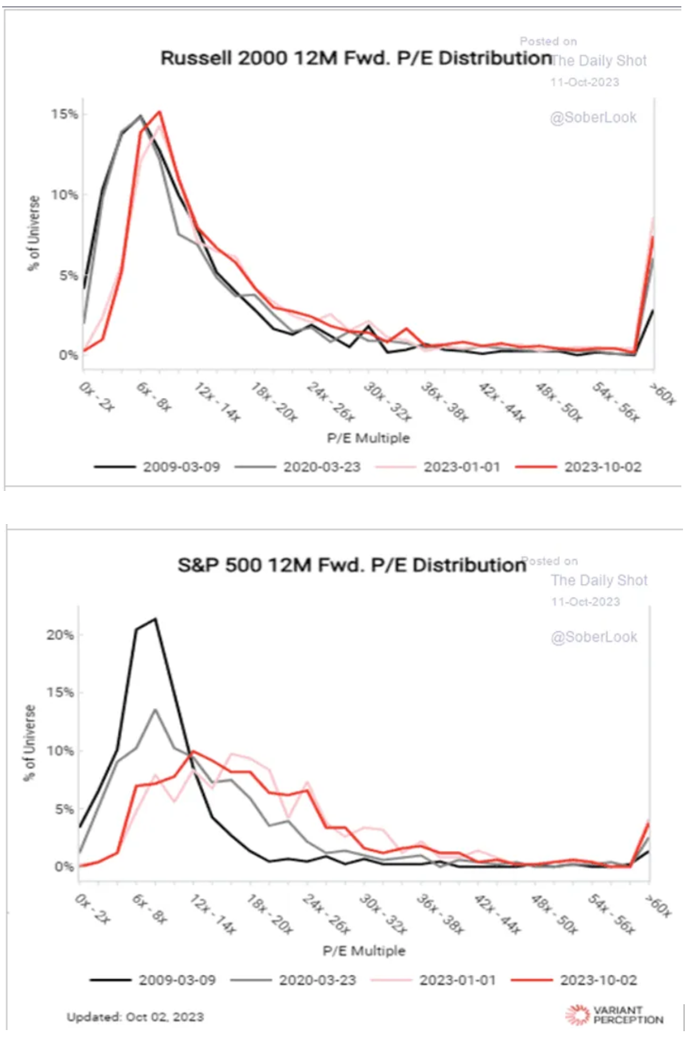

While we are not fans of the Russell 2000 inclusion methodology (we much prefer the S&P 500), one can see that the current forward PE distribution of the index is starting to resemble the distributions of recent market lows, contrary to the S&P 500.

We said earlier that workers were going to ask for a bigger slice of the revenue in the future.

Governments are likely to do the same… The marginal voters will soon cease to be baby boomers and will be cash and asset poor favoring redistribution policies financed through higher taxes.

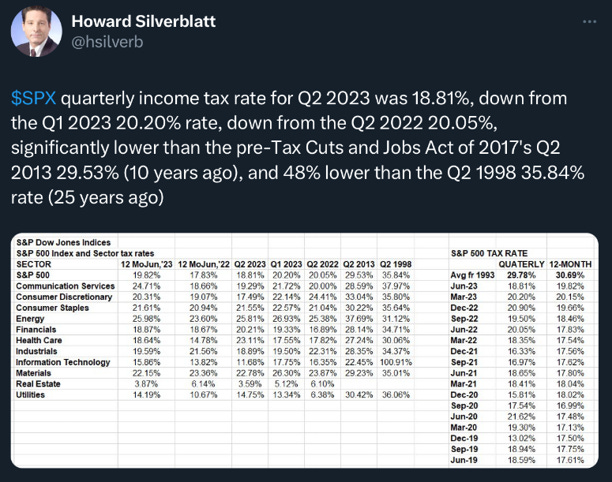

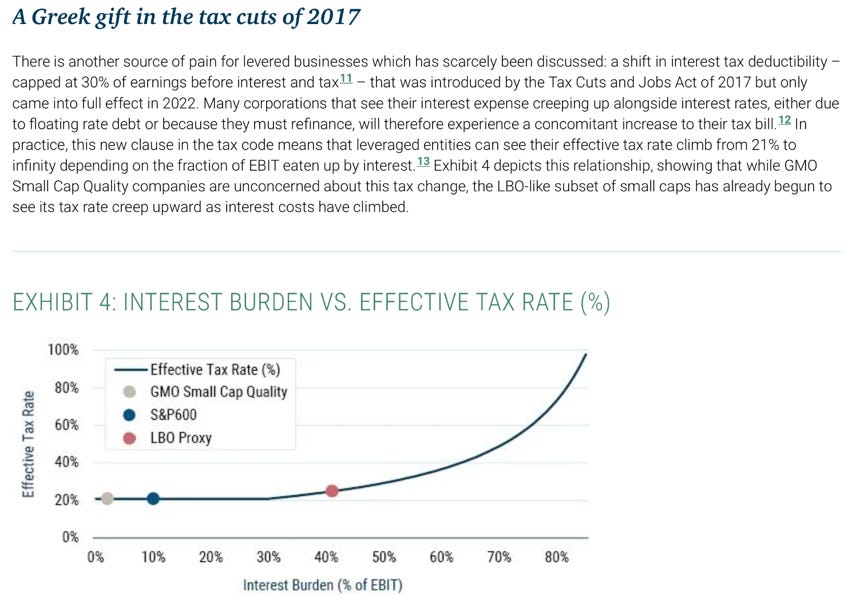

In the meantime, from GMO…

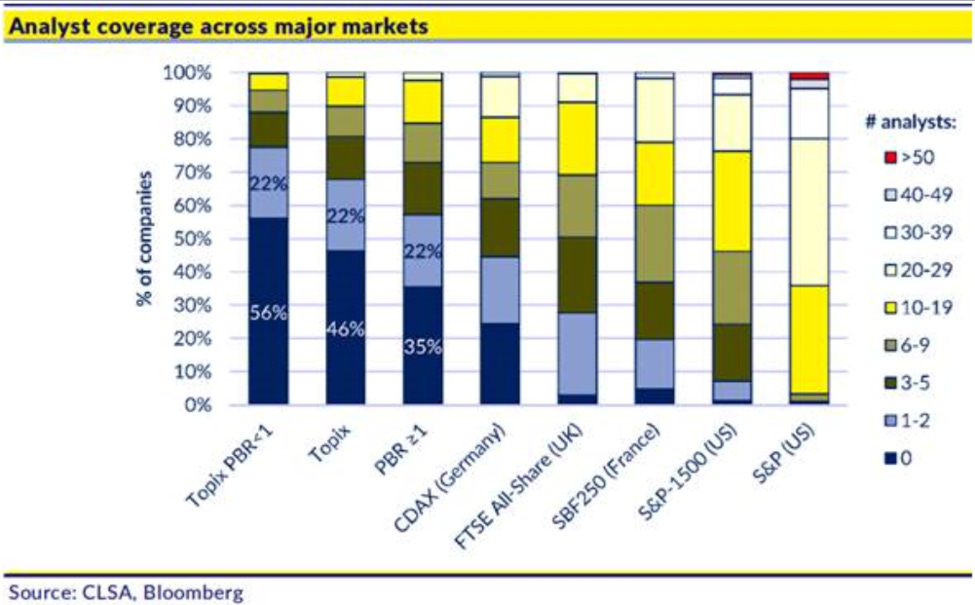

Market - Japan

Another reason to like Japan… lots of “undercovered” stocks!

Others

Flight to quality?

Larry, please… Some years ago you were saying this…

Of course, only fools do not change their mind but here it feels a bit… opportunistic.