US Market Valuation: One for the History Book?

The notebooklm audio overview

Executive Summary

This analysis presents a sobering outlook for the S&P 500, arguing that it is currently the most overvalued it has ever been, surpassing even the 2000 Tech Bubble and 2021 market frenzy. Key points include:

The Margin-Adjusted Cyclically-Adjusted Price Earning Ratio (MAPE) indicates extreme overvaluation.

Projections suggest negative nominal total returns for the S&P 500 over the next 10 years, with potential annual losses of 1.4% to 8.9%.

A market correction to historical valuation norms could result in substantial losses, potentially up to 21.4% annually if occurring within the next three years.

Ultra-loose monetary and fiscal policies have contributed to market distortion and speculation.

Current market behavior reflects complacency and diminished critical thinking among investors.

The analysis warns of potential inflationary pressures and the need for investors to reassess risk tolerance and prepare for lower returns or significant drawdowns.

The article concludes that achieving positive real returns in the coming decade would require exceptional circumstances, urging investors to remain grounded in fundamental valuation principles.

“Value investing is at its core the marriage of a contrarian streak and a calculator.”

S. Klarman

“The first principle is that you must not fool yourself, and you are the easier person to fool.”

R. Feynman

In this analysis, we aim to objectively examine the current discrepancy between the intrinsic value and the market price of the S&P 500.

Our conclusion is that the S&P 500 is unlikely to have a positive nominal total return in the next 10 years and a ‘miracle’ would be needed to achieve positive real total returns.

Central Banks have brought forward future equity returns (and some more) with their accommodative policies and hyper-sensibility to downside volatility. Ultra-loose fiscal policies since Covid (justified in the first 6 months not thereafter) have put gasoline on the fire.

Being blunt, there is a real possibility for the S&P 500 to revisit at least the 2020 lows in the coming years.

Before we dive in, it's important to recognize that valuation metrics have little to no ability to predict short-term market fluctuations. Think of it like a rubber band: the farther the market price is from its intrinsic value, the stronger the pull back toward that value. This means that even seemingly insignificant events can trigger the start of a mean reversion when valuations are extreme.

Market Behavior and Investor Psychology

When equity markets appear unstoppable—rising relentlessly on good, bad, or no news—investors may neglect the fundamental principle that value anchors price.

Over a decade of quasi-invincibility, where every market decline is swiftly recovered, can lead to complacency and diminished critical thinking. Reflection becomes a liability. The educated fools are in control.

This environment fosters narratives like "Buy the Dip," and the creation of viral acronyms such as BTFD (Buy The F***ing Dip), FOMO (Fear Of Missing Out), and HODL (Hold On for Dear Life).

This time it is really different! Is it?

Central Banks around the world, by lowering interest rates aggressively and providing unlimited support, verbally and/or materially, to the markets at the slightest emergence of stress and by taking too much time or even refusing to remove the accommodations they provided, have set the stage for historical markets and social dislocations.

If one add that a chunk of the post-Covid fiscal spending largess going directly to the equity markets through gamified trading applications or passive mom and pop vehicles or the emergence of the YOLO meme/life mantra you have all the ingredients for a massive speculation frenzy.

When finance dominates everything, when companies' management are obsessed by financial engineering and short-term personal rewards, when governments/central banks/regulators are controlled and not controlling, dogmatic and not pragmatic, the end result cannot be good.

While we will expand on this in another article, Ben Hunt of Epsilon theory has written extensively and brilliantly on the subject. One could start here.

Bubbles need leverage to expand

Although central banks have rapidly increased their target rates—often belatedly—they are now swiftly reversing course, once again demonstrating their asymmetric reaction functions.

Interest rates below a certain level probably have a detrimental effect for the real economy as investments in new productive capital become less and less elastic to rates as they decline toward 0%.

Zombie companies survive, preventing any Schumpetarian creative destruction, leaving excess supply in place, pushing inflation rate down (what? low rates could be deflationary?).

Furthermore, savers are forced to spend less unless they take more risk as their fixed income portfolio doesn't generate much of an income.

The only thing striving is finance where actors put on more and more leverage to buy existing capital (buybacks, M&A, dividend payment to private equity firm, etc).

The sad consequence is a larger stock of debt unbacked by new productive capital.

A system where overall debt cannot be repaid, ever. A system where the can is kicked down the road until it can't anymore.

The end game is either an inflationary burst to save the debtors, a multi-decade's slow growth environment or a deflationary burst.

Given that the debtors are governments, interest groups lobbying them and Generation X and the younger ones (who will soon dominate the electorate), we have little doubt that the inflationary scenario is the most probable.

But let's come back to the main subject of this article, the US equity market valuation.

Stocks are a claim on a expected future stream of cash flows. To assess this stream's value today, we have to calculate its present value using an appropriate discount rate. This present value is called the intrinsic value of a stock or of a group of stocks.

At a given discount rate, the short-term fluctuations of cash flows have very little influence on intrinsic value. Remove entirely 1 or 2 years of cash flow and the difference will be small.

Longer-term expectation, on the other hand, have a large impact. Those expectations are highly pro-cyclical.

Earnings are already, as we will shortly demonstrate, well above trend and, therefore are highly likely to grow less than the overall economy. Still analysts are expecting them to grow much more quickly.

Changing the discount rate can have a huge impact.

Discount rate assumptions backed by market participants are strongly correlated with their mood. Bullish participants will accept a lower discount rate, ceteris paribus.

Prevailing interest rates usually serve as a loose anchor to discount rate assumptions. We can nevertheless see, experimentally, an increased exposure to risky assets the lower the risk-free rate is, even when the mean excess return is the same.

On the graph below, one can see the average allocations to a risky asset across different interest rate conditions. Each condition has 200 participants, from the MTurk platform. The x-axis shows the risk-free rate in each condition. The mean excess return on the risky asset is 5% in all conditions.

We will now demonstrate using a methodology proposed by J. Hussman, the Margin-Adjusted Cyclically-Adjusted Price Earning Ratio (MAPE), that the US stock markets is the most overvalued it has ever been.

R. Shiller and J. Campell proposed the concept Cyclically-Adjusted Price Earning (CAPE) to forecast 7-12 years markets future return using a long moving average of earnings back in 1988 (originally 10 years). The goal was to smooth out the business cycle influence on earnings in order to get a smoother series they called trend earnings.

The CAPE model was good at forecasting forward return in the past (M. Faber applied it to foreign markets too) but some argue that accounting changes, payout policies, a move toward less competitive markets could have made the CAPE model lose some or even most of its forecasting ability.

One can find some great discussion on the subject here and here.

R. Shiller introduced the Cyclically-Adjusted Total Return Price Earning Ratio to account for the change in company payout policies with the increased use of buybacks to return capital to shareholders.

Two flaws remained nevertheless.

First, as identified by J. Hussman, one can get an even smoother trend earning series by adjusting the CAPE to get constant historical margins. He uses 5.4% margin as its average. So if the most recent 10 years average margin is 7%, one ought to multiply the CAPE by 7%/5.4% (1.3). A CAPE of 30 becomes a MAPE of 40.

The second problem is that margin could have increased permanently due to structural change in the economy and the dominance of capital-light businesses.

While this might explain some of the increase in margin, we are convinced that a large part of the increase in margin is transitory and that once capitalism is allowed to work as it should, it will disappear. It will be the subject for another article.

Anyhow, we have assumed a permanent increase of margin to 7% starting in 1998 with the emergence of internet.

Let's now look at the data.

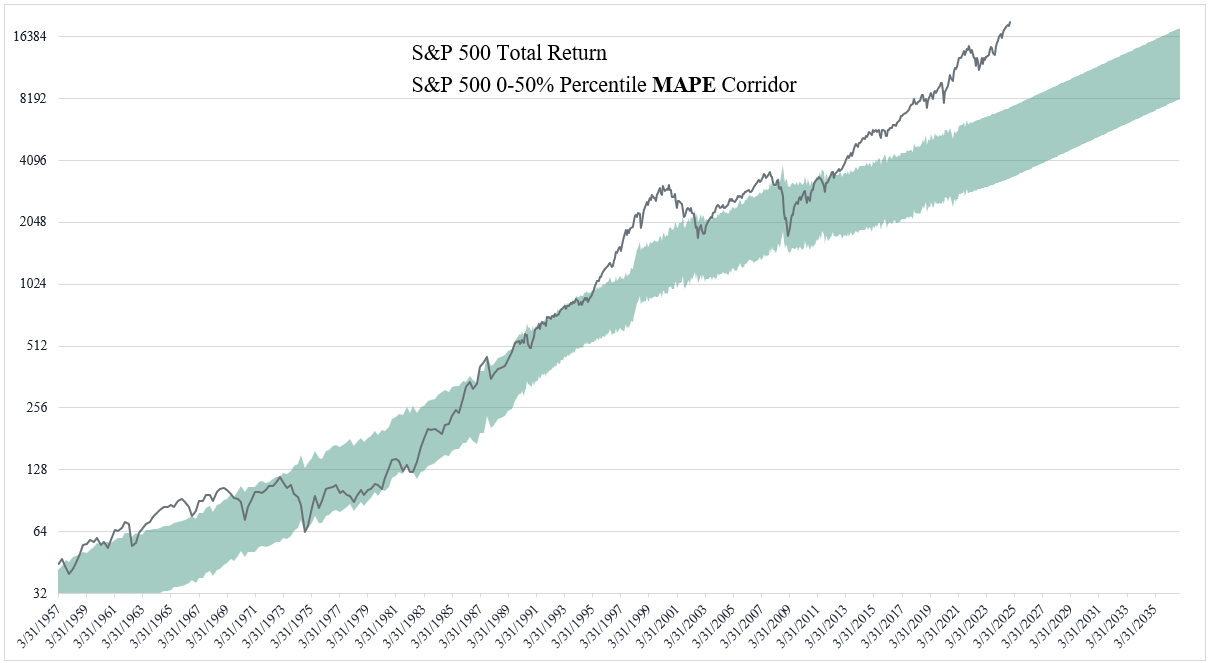

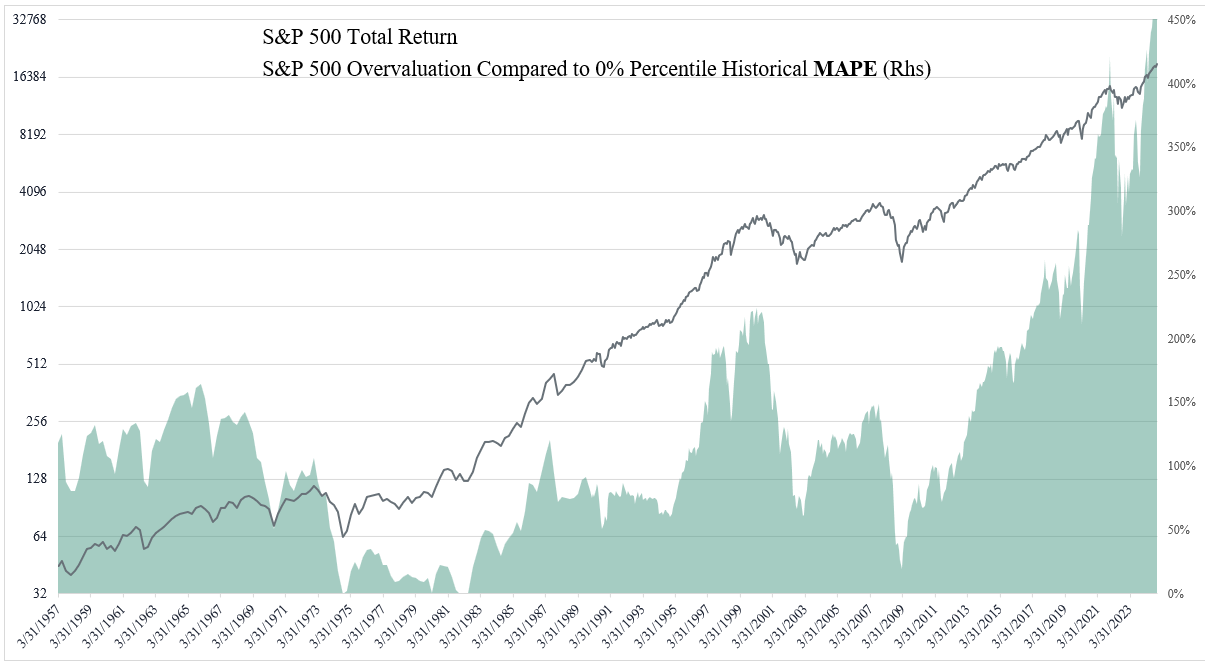

As one can see, today's MAPE is the highest it has ever been, dwarfing the 2000 Tech Bubble and the end of 2021 frenzy.

We won’t talk about the divergence on factor valuations here, it will be the subject of another article.

If we construct an historical corridor with boundaries between the 0% and 50% percentiles of MAPE history, the prospect looks grim for Buy and Holders.

If we construct an historical corridor with boundaries between the 0% and 50% percentiles of MAPE history, the prospect looks grim for Buy and Holders.

The S&P 500 is currently almost 400% above the level corresponding to a bottom MAPE and 130% above the 50% percentile MAPE history.

If we assumed a return to the MAPE 50% percentile, with nominal trend earnings growing at their historical pace and the current 1.26% dividend yield, one can see that the S&P 500 nominal total return for the next 10 years would be at -1.4% annually.

If the markets reached similar valuation to the summer 1982, the nominal total return for the next 10 years would be at -8.9% annually.

We doubt (and it is a strong understatement) the markets will wait 10 years to test the MAPE 50% percentile. A retest in the next 3 years is possible. Reaching the MAPE 50% percentile in 3 years’ time would imply an annualized 21.4% loss.

Even if we assume normalized margins to be 10%, a return to the MAPE 50% percentile in 3 years’ time would imply an annualized loss of more than 15%!

One should also not forget the historical tendency of deeply overvalued markets to fall significantly below the MAPE 50% percentile.

It is also important to remember that today's margins are above our 7% assumption and that the CBO is projecting around 4% nominal US GDP growth to 2034. The odds are thus stacked against the >6% nominal earning growth we have assumed.

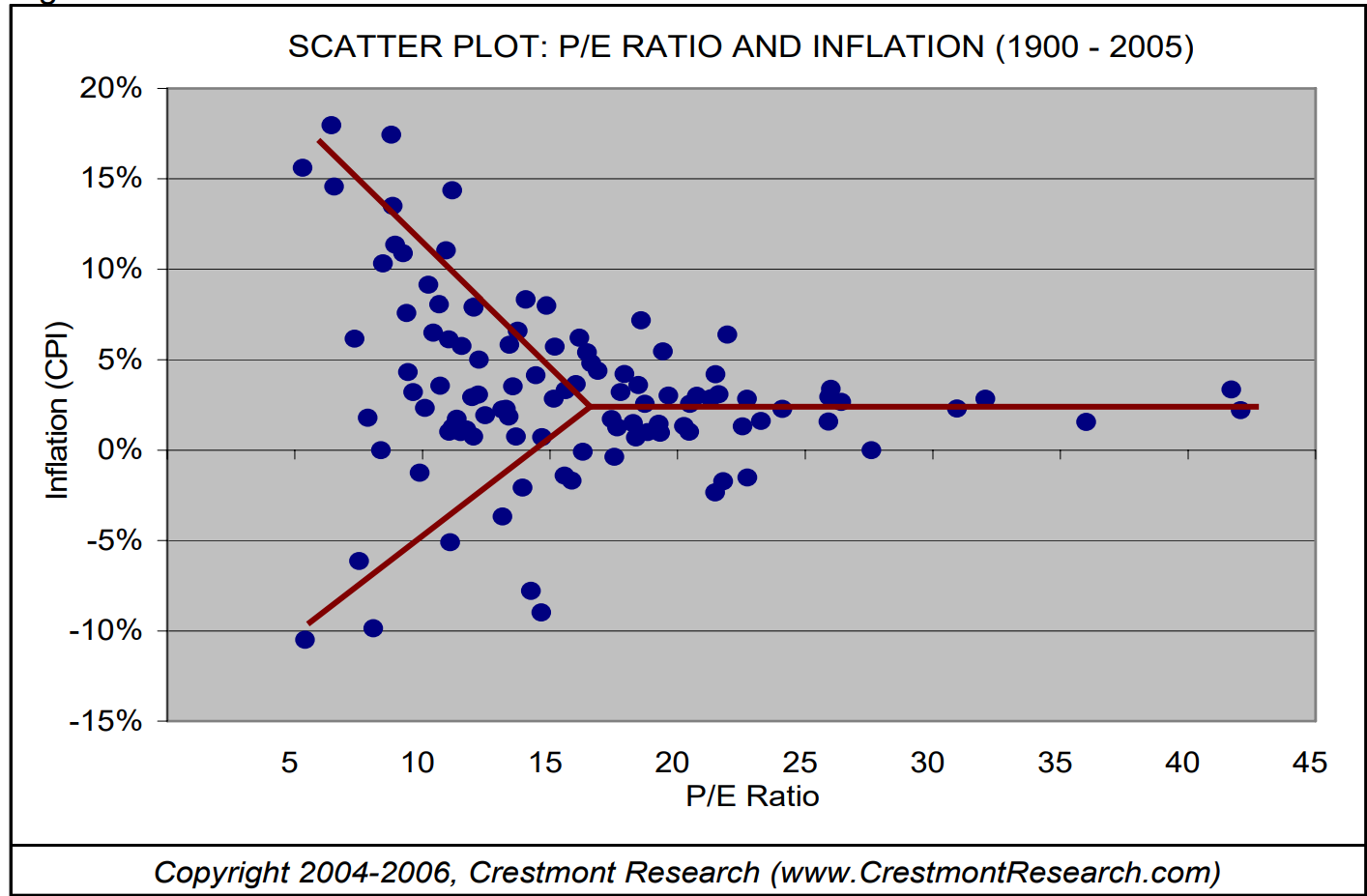

Among all the factors which will impact the markets nominal total return, the most important is inflation. As we have said earlier, on a 10-20 years’ basis the politicians' rulers and their electors will favor much higher level of inflation.

In this scenario, while nominal earning growth will be higher, ceteris paribus, with increasing inflation, the price investors will be willing to pay for each unit of earning will decline. Investors do not like inflation or deflation.

Conclusion

In light of our analysis, the current state of the S&P 500 presents a sobering outlook for investors. The unprecedented levels of the Margin-Adjusted Cyclically-Adjusted Price Earning Ratio (MAPE) signal a market that is significantly overvalued, even surpassing the extremes of the 2000 Tech Bubble and the 2021 market frenzy.

Our projections suggest that achieving positive real returns in the coming decade would require nothing short of a miracle. The combination of ultra-loose monetary policies, misaligned fiscal measures, and a pervasive "this time is different" mentality has created a perfect storm of market distortion.Investors should be acutely aware that:

The S&P 500 is currently trading at levels that are unsustainable in the long term.

Even with optimistic assumptions, the potential for negative returns over the next 10 years is significant.

A market correction to historical fair value could result in substantial losses, potentially as high as 21.4% annually if occurring within the next three years.

As we navigate these treacherous waters, it's crucial to remember the wisdom of Seth Klarman: "Value investing is at its core the marriage of a contrarian streak and a calculator."

Now, more than ever, investors must resist the siren song of market euphoria and anchor their decisions in sound valuation principles.

The road ahead may be challenging, but it also presents opportunities for those who maintain discipline and a clear-eyed view of market fundamentals.

As we face the possibility of increased inflation and potential market turbulence, prudent investors should reassess their risk tolerance, diversify wisely, and prepare for a period of lower returns or even significant drawdowns.

In closing, let us heed Richard Feynman's caution against self-deception. The markets have a way of teaching harsh lessons to those who ignore the fundamentals.

By staying grounded in reality and maintaining a long-term perspective, investors can navigate the coming years with greater resilience and potentially position themselves to capitalize on the opportunities that inevitably arise when markets return to more rational valuations.

"It is better to be out of the markets wishing to be in than in the markets wishing to be out" Unknown

“I never invest at the bottom, and I always sell too soon.”

Nathan Rothschild

Disclaimer

The views and opinions expressed in this post are solely those of the author. This content does not reflect the views or positions of any entities where the author works or is contracted from.

This stock report is provided for informational purposes only and represents the author's personal opinions based on research and analysis conducted at the time of writing. The information contained herein should not be construed as financial, legal, or investment advice.

Not a Recommendation: This report does not constitute a recommendation to buy, sell, or hold any security or financial instrument. Any action taken based on the information presented is at the reader's own risk and discretion.

Do Your Own Research: Readers are strongly encouraged to conduct their own due diligence and consult with qualified financial advisors before making any investment decisions. The author is not responsible for any actions taken based on the information provided in this report.

No Guarantee of Accuracy: While efforts have been made to ensure the accuracy and reliability of the information presented, the author makes no representations or warranties of any kind, express or implied, about the completeness, accuracy, reliability, suitability, or availability of the information contained in this report.

Past Performance: Any references to past performance of securities or markets are not indicative of future results. Investments can go up or down in value, and there is always the potential for loss as well as profit.

Forward-Looking Statements: This report may contain forward-looking statements that are based on current expectations, forecasts, and assumptions. These statements involve risks and uncertainties, and actual results may differ materially from those expressed or implied.

Conflicts of Interest: The author may hold positions in the securities discussed in this report. Readers should be aware that the author may have a conflict of interest that could affect the objectivity of this analysis.

Not Tailored Advice: This report does not take into account the specific investment objectives, financial situation, or particular needs of any individual person or entity. It is not personalized advice or a solicitation for any specific investment product or service.

Subject to Change: The opinions and information presented in this report are subject to change without notice.. The author is under no obligation to update or amend this report based on new information, future events, or for any other reason.

Jurisdiction: This report is not directed to, or intended for distribution to or use by, any person or entity who is a citizen or resident of or located in any locality, state, country, or other jurisdiction where such distribution, publication, availability, or use would be contrary to law or regulation.

By accessing and reading this stock report, you acknowledge that you have read, understood, and agree to be bound by the terms of this disclaimer.

I am in awe of your commentary. This is a high quality read and intend to make time to absorb this fully. Thanks as ever for your work!

This is excellent work! Thank you